Let’s begin by asking the most pressing question: why is a TCPA compliance checklist important?

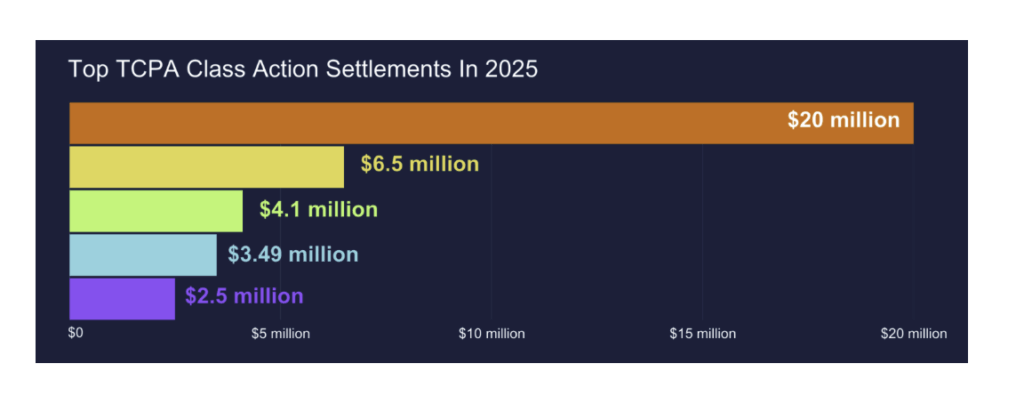

Political campaigns risk TCPA violations for every unauthorised call or text, especially with surging class action lawsuits and hefty penalties per infraction. Recent increases in enforcement, with 2025 seeing over double the number of cases filed in the previous year, make consistent and thorough compliance non-negotiable.

Our TCPA compliance checklist ensures campaigns avoid legally risky mistakes, such as contacting unconsenting voters or making calls outside permissible hours. This maintains transparent and respectful communication, protecting reputations and funds from fines and litigation.

The latest TCPA compliance checklist: Rules and updates

Before diving into the checklist, here are the key changes shaping compliance this year:

10-day opt-out rule:

All opt-out requests (by text, call, email, mail, or verbal statement) must be processed within 10 business days instead of 30.

Expanded opt-out methods:

In 2025, voters can revoke consent in many ways, not just by texting “STOP”. Informal replies like “unsubscribe” or “don’t text me,” verbal requests on calls, emails, and even website forms all count.

CallHub makes this easy by recognizing multiple opt-out phrases, letting agents mark contacts as “Do Not Call” instantly, and syncing those opt-outs across all campaigns so no one gets contacted again by mistake.

Opt-Out Revocation Rules

Starting April 11, 2025, businesses must honor opt-outs in any reasonable manner and must stop sending calls or texts within 10 business days of receiving a revocation request. In some cases, especially when a revocation is made in response to an informational message, that revocation already must extend to all robocalls and robotexts.

The requirement that any revocation in one channel or message type automatically apply to all future automated outreach(calls, texts, etc., including unrelated messages) has been delayed until April 11, 2026, giving businesses extra time to adjust systems.

Stay compliant by enabling auto STOP handling and syncing opt-outs to your Do Not Call (DNC) list in CallHub.

AI-generated robocalls:

Under the TCPA rules, AI-generated or deepfake voices in robocalls are illegal. Make sure you are using human-recorded audio for robocalls.

Read Also: Your Complete Phonebanking Compliance Guide For The U.S, E.U., & CA.

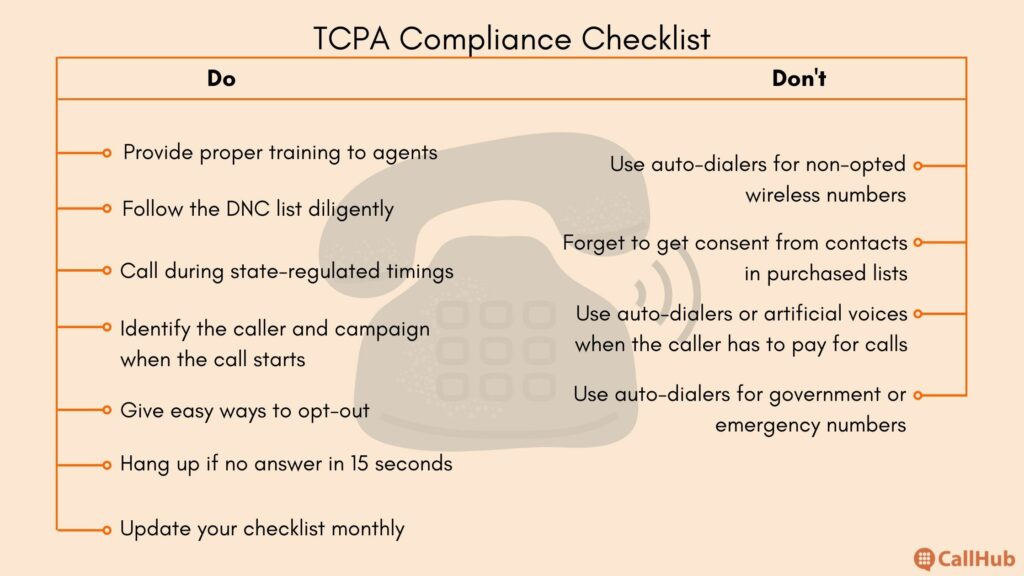

TCPA compliance checklist: Best practices in 2025

Compliance starts with what you do legally when running calling or texting campaigns. The rules apply whether you have five volunteers or five hundred working the phones.

Train your agents on the TCPA compliance checklist

The more volunteers you onboard, the higher the risk of someone breaking a rule. Make TCPA training mandatory:

Honor your DNC list

While political campaigns are exempt from the national DNC, you must maintain and respect your own DNC list. Anyone who opts out of your calls or texts.

With CallHub, you can:

- Mark a call disposition like “Do Not Call”, “Not Interested”, or “Bad Number”.

- Automatically weed out contacts from future campaigns.

- Stay protected from lawsuits over unwanted follow-ups.

Read Also: Mobilize The Workforce: How You Can Use Calling For Unions.

Call only during state-approved times

The TCPA guidelines mandate calling contacts only between 8 a.m. and 9 p.m. in the recipient’s location. However, some states have their own approved timings within this bracket. Make sure you stay within those limits. For instance:

- Alabama and Mississippi: 8 a.m. – 8 p.m., Mon – Sat; no calls on Sundays.

State-wise calling timings that are more restrictive than TCPA:

When you try to adhere to these timings without automation, you risk overscheduling (e.g., if you call within the time bracket in your time zone but the recipient lives in a location a few hours ahead).

To prevent such accidents, use call center software like CallHub to:

- Automatically adjust for local time zones.

- Stop campaigns the moment hours expire.

- Prevent accidental violations.

Read Also: Your All-In-One Guide To Conversational Text Messaging.

Identify yourself at the start of every call

This isn’t just courtesy; it is also a TCPA mandate that requires callers to identify themselves at the beginning of the conversation. Your call needs to begin with identifying yourself, the organization you represent, and the purpose of the call.

Write a phone banking script that covers the introduction well and ensures no agent misses this crucial part of the conversation.

TCPA mandates that every call must open with:

- Identity disclosure: This includes the name and designation of the caller, and the identity of the organization/campaign.

- Purpose of the call: Whether you are calling for donations, voter profiling, or GOTV, the purpose of the call needs to be stated clearly and towards the beginning of the call (before you get the information you need or ask questions related to the purpose).

- Information about opting out of further communications: You must provide easy ways to opt out if a person does not wish to be contacted by you. They must be able to do so verbally (mention this on the call) or in writing (text an opt-out keyword to your number). In both instances, you must immediately add the person to your campaign’s DNC list.

- CallHub simplifies this with automated DNC suppression: once a voter opts out, their number is removed from every active and future campaign.

Sample script:

Hello, [contact’s name]; this is [agent name], an outreach specialist with the [candidate name] campaign. [Candidate name] will address a rally on St Mark Street on October 17th and speak with supporters regarding our economic policy for new small businesses. If you’d prefer not to receive calls from us, just let me know.

Read Also: Write The Easiest Fundraising Cold Call Script (With Samples)

Provide easy opt-out options

Voters must be able to revoke consent in any reasonable way (a new rule in 2025). This includes:

- Verbal opt-outs on a live call.

- Written opt-outs (letters, emails).

- Electronic opt-outs (keyword in text, website forms).

The campaign now has 10 business days (down from 30) to process these requests. With CallHub, opt-outs can be logged instantly through call dispositions.

Hang up if there’s no answer within 15 seconds

Hanging up within this timeframe isn’t a legal requirement, but still a best practice followed by telemarketers and political campaigns. Stop a call ringing without an answer for 15 seconds ( about four rings).

- Saves volunteer time.

- Prevents voter frustration from repeated hang-ups.

- Lets you retry later with better chances of success.

Read Also: Political Calling Made Easy: Top Features For Your Calling Campaign.

Update your TCPA compliance checklist monthly

TCPA rules evolve (typically during election season). To keep up with the changed norms, it’s advised to go through the rules every month and update your checklist accordingly.

Make sure to retrain volunteers and update your process accordingly.

You can keep a check on the rules on the FCC (Federal Communications Commission) website or ask your legal counsel to do a thorough check and inform your communications team.

Read Also: Robocall Laws: What New FCC Rules Mean For Politicians, and inform your communications team.

TCPA compliance checklist: What is prohibited?

While understanding what you should do is important, knowing the “don’ts” of TCPA is critical. These prohibitions should be treated as high-priority items in every campaign’s compliance checklist.

No auto-dialing wireless numbers without consent

- You may not use automated dialers to call or text wireless numbers (cell phones, pagers, etc.) unless the recipient has given express written consent.

- This restriction applies to both live calls and prerecorded/artificial voice calls.

You can use automated dialers for:

- Wireless numbers with prior opt-in.

- Landlines or wired numbers (opt-in not required for live calls).

No calls without valid consent beyond four years

- Consent is not permanent.

- Voter consent to receive auto-dialed calls, prerecorded messages, or texts lasts for four years.

- After that, you must request renewed permission.

No “Cold” automated outreach to purchased lists

- Purchased voter files or contact lists do not count as consent.

- Your first outreach must be manual, via hand-dialed calls or individually sent texts.

- Only after a person opts in can you add them to automated campaigns.

- Best practices here include blending early campaign conversations with a clear opt-in request (e.g., “Can we send you campaign updates by text?”).

Read Also: Manual Dialer: Here is What the New Law says.

- If the recipient is paying for the call, no recording is permitted. TCPA prohibits using autodialers or prerecorded, artificial voices for calls where the recipient bears the cost.

- This applies to toll-free numbers such as: 800, 888, 877, 886, 855, 844, 833, etc.

- Always scrub your lists to remove toll-free numbers before launching automated outreach.

No auto-dialing emergency or government lines

Do not contact through autodialers or recordings:

Numbers assigned to emergency cellular or paging services.

Emergency lines (police, fire, poison control, etc.).

Patient or guest rooms in hospitals or healthcare facilities.

Quick takeaway from TCPA compliance checklist

TCPA prohibitions are non-negotiable.

- No automated outreach without consent.

- No consent older than four years,

- No relying on purchased lists without first getting opt-ins.

- No call where the recipient pays.

- No autodialing emergency or restricted lines.

Following these “don’ts” is just as important as following the “dos”. Together, they form the backbone of a campaign’s TCPA compliance checklist.

Read Also: Messaging Compliance: Prohibited Practices & How to Stay Safe

To Conclude:

To scale outreach without risking fines, campaigns need an actionable TCPA compliance checklist that reflects the latest 2025 rules. Optimize every step for clarity, transparency, and rigorous documentation, while leveraging campaign management tools that support these goals.

Fines aren’t fun. Voter conversations are. Choose the fun part — start your compliant campaign with CallHub today.

FAQ: TCPA compliance checklist questions

What is TCPA compliance?

TCPA compliance means following the Telephone Consumer Protection Act (TCPA) rules that protect people from unwanted calls and texts. For you, it simply means making sure your outreach campaigns only reach people who’ve given you permission — the right way, at the right time.

What is required for TCPA compliance?

To stay compliant, you’ll need to: Get clear permission (consent) from people before sending automated calls or texts. Provide an easy opt-out option (like replying STOP) . Respect the National and Internal Do Not Call (DNC) lists. Only reach contacts during allowed hours (8 a.m.–9 p.m. local time generally varies state to state). With CallHub, these safeguards are built into the platform — making compliance easier for you.

What are the penalties for non-compliance with the new TCPA rules?

Penalties for violating TCPA can be steep: Up to $500 per violation, and up to $1,500 if the violation is willful. These fines are per call or text, and class-action lawsuits can rapidly multiply costs. For example, a TCPA class action involving 1.8 million violations resulted in fines nearing $925 million.

What is TCPA text messaging compliance?

This refers to following TCPA rules when sending SMS or MMS campaigns. You must: Secure prior express written consent before sending marketing texts. Clearly explain what recipients will receive and how often. Include an easy opt-out in every message. Stick to the allowed sending hours.CallHub helps enforce these guidelines automatically, so you stay compliant effortlessly. Dive deeper here: TCPA regulations for text messages

What does TCPA compliance mean?

TCPA compliance means running your campaigns in a way that’s legal, respectful, and safe, protecting both your organization and your contacts. With CallHub, all of these protections are built right into your campaign tools.